After a summer that offered a glimmer of stability, September revealed a marked deterioration, with exports dropping a significant 12.4% year-on-year. The total value of these exports stood at CHF 2.1 billion, but beneath this figure lies a narrative of troubling shifts, especially in key Asian markets, raising concerns about the industry’s trajectory as the year draws to a close.

The September export figures mark the sharpest monthly decline in 2024. This wasn’t just a momentary hiccup, it reflects a broader trend of weakening demand, with export turnover for the year’s first nine months falling by 2.7% compared to the same period in 2023.

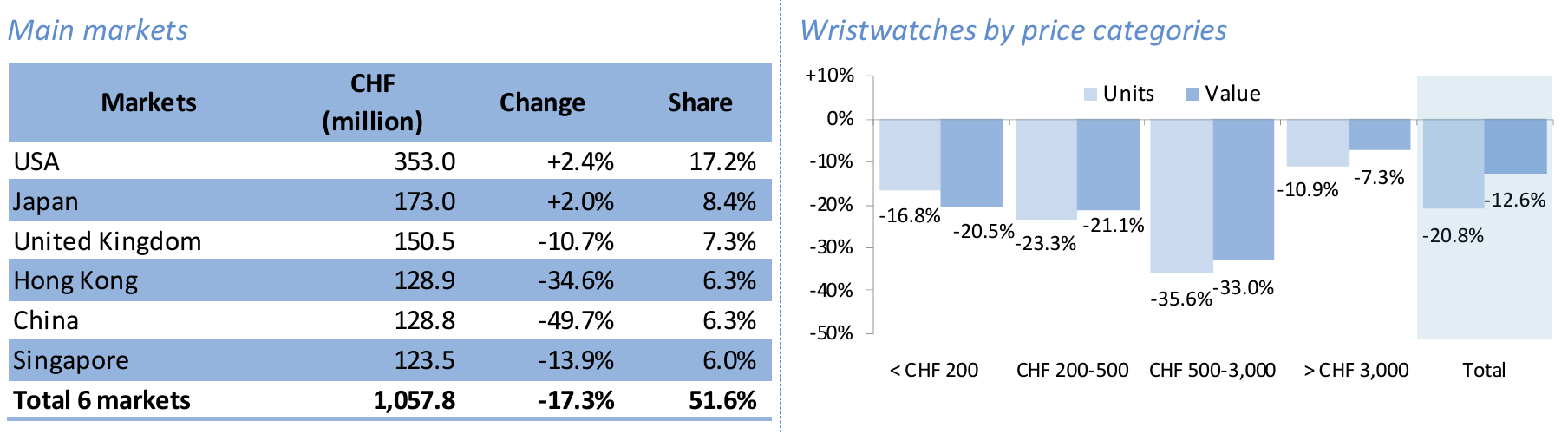

The geographical breakdown of the data tells much of the story. A sharp slowdown in China and Hong Kong, traditionally among the strongest consumers of Swiss luxury watches, accounted for two-thirds of the overall export decline. China, in particular, saw exports fall by a staggering 49.7%, while Hong Kong registered a 34.6% drop. These numbers are not just a reflection of slowing demand but perhaps also indicative of wider economic headwinds in the region.

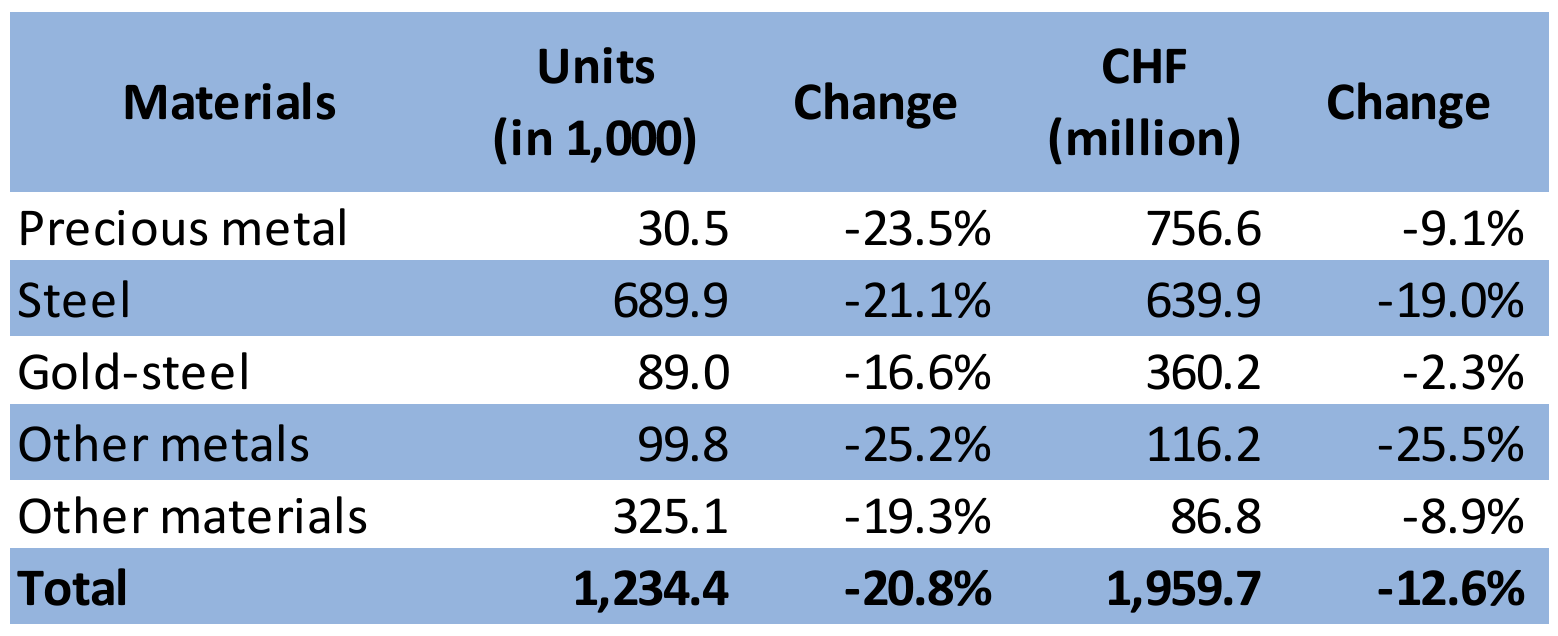

The performance across materials tells an equally compelling tale. Steel, often seen as the backbone of Swiss watch manufacturing due to its versatility and widespread appeal, was disproportionately affected. Exports of steel watches fell by 19.0% in value and a more alarming 21.1% in the number of units shipped. While steel watches span a wide range of price points, they are particularly prominent in the mid-market luxury segment—a space that has recently faced increasing pressure.

Watches crafted from precious metals fared slightly better but still saw a 9.1% decline in value. The premium sector, which includes gold and platinum timepieces, remains essential to maintaining Swiss watchmaking’s prestigious image. However, the cooling demand for high-value luxury items, especially in price-sensitive markets, seems to have weighed on this segment too.

In volume terms, other materials and metals plummeted. The “Other materials” category dropped by 19.3%, while “Other metals” saw a more severe 25.2% decline, together accounting for a third of the overall volume reduction.

One of the more striking aspects of the September data is the uniform decline across all price segments, though the extent of the fall varies widely. The hardest hit were watches priced under CHF 500 (export price), which saw their value drop by 20.8%. Watches in the CHF 500 to CHF 3,000 range—often considered the heart of the aspirational luxury segment, declined even more dramatically, with a 33.0% fall in export value. I can’t recall the last time I had to write about such declines in the past couple of years..

Asia has been the engine of focus and growth for the Swiss watch industry for much of the past decade. However, in September 2024, the region posted its worst performance of the year. Exports to Asia fell by a whopping 22.6%, dragged down primarily by China, Hong Kong, Singapore (-13.9%), and Taiwan (-29.8%).

China’s export contraction of 49.7% is particularly striking and alarming. I’m guesstimating that this isn’t just about the Chinese government’s tighter economic policies but also the country’s slower-than-expected economic recovery. Additionally, China’s broader real estate and economic challenges have possibly left wealthy individuals rethinking discretionary purchases.

Hong Kong, long a critical gateway for Swiss watchmakers into China and the broader Asian market, saw a 34.6% decline in exports. Political and economic uncertainty, compounded by shifting trade dynamics, has (for a while now) reduced its importance as a luxury shopping hub.

Other parts of Asia also reported significant contractions. South Korea (-19.8%), Taiwan (-29.8%), and Thailand (-34.6%) are key players in the regional luxury market, but the region’s overall economic slowdown has clearly affected demand for high-end timepieces.

While Asia is grappling with a severe downturn, Europe’s picture is more mixed. Overall, exports to Europe fell by 3.4%, but this was primarily due to sharp declines in the UK (-10.7%) and several smaller markets. However, Germany (+5.7%) and Spain (+5.3%) offered a rare bright spot in an otherwise gloomy landscape. Both countries have benefited from strong consumer sentiment, as well as a boost in domestic spending on luxury goods. The United States continued its upward trend, with exports rising by 2.4%, cementing its position as the top destination for Swiss watches. The U.S. market, driven by a combination of robust consumer spending and a resurgent luxury sector, has become increasingly critical to Swiss watchmakers.

The resilience of the U.S. market and pockets of strength in Europe suggest that there is still robust demand for Swiss craftsmanship. Moreover, as inflationary pressures ease in certain regions, consumer spending may pick up in 2024, especially in high-income segments.

Graphs provided by the Federation of the Swiss Watch Industry